Always Be Replacing

An accidental treasurer

For the past five years, my wife and I have lived in Oakland, just across the Bay from San Francisco. Before we moved, we had an awesome apartment—a corner unit overlooking a courtyard in a converted hotel, with neighbors who bought us a pizza the day we moved in, and a beautiful fountain in the courtyard. We were sad to move, but with kids on the horizon, we needed something a bit bigger, and took a chance on a condo not far from our old place.

I still remember the initial tour—the agent, Sherie, remarked that it “felt straight out of New York”: a two-level unit on the twelfth floor, near the end of a rat maze of narrow, white-walled corridors. The building was vast: 328 residences over 15 floors, with 20 ground-level shops including everything from Citibank to a ginseng boutique. Situated across an entire city block in Oakland, the structure was a self-contained city, with a private second-floor garden and 400 underground parking spaces. An American might say “New York,” but I visited Hong Kong a few years after we moved in, and it’s a dead ringer, down to the morning market that takes over the sidewalk every Friday morning.

Friday morning market. Image courtesy of the author.

Land use comes up a lot at Strong Towns—I live on 1/350th of a city block, some 140 feet in the air. That’s not without challenges: three-phase electricity for elevators and garage fans, 24/7 booster pumps lifting water hundreds of feet to the upper floors, and the financial infrastructure—budgeting, invoicing, collections—to keep it running. I got to know the management and before long I was on the board, as treasurer.

I didn’t realize it at the time, but with 800 people, I was running a small town—with exactly the problems Strong Towns predicts. We were drowning in deferred maintenance, and didn’t even realize it.

How it’s supposed to work

At first glance, everything looked OK—minimal delinquency, no debt on the books. Great!

Except…we’d just done a large waterproofing project, and owed the vendor nearly $800,000, for which we were paying $33,000/month…not recorded anywhere. The Association was treating this money as if we were spending it—and theoretically, getting something for it—every month, years after the work was done. Lies! Keeping that debt off the books was problem #1. But there was more: a short-term loan to pay our insurance premium which, while less bad than the waterproofing (it would be paid within a year), still made it difficult to see the organization’s financial position.*

[*Technical accounting note: if you understand accrual-basis accounting, yet insist on using cash-basis to run a city, you’re a menace to society. Seek atonement from the AICPA, and book those liabilities.]

A cracked flue pipe leaking exhaust gas from a boiler. Image courtesy of the author.

The bigger issue, problem #2, was our replacement liability. Following California law, we’d contracted for a “reserve study”—a detailed inventory of the building’s contents, with estimated replacement dates, and costs. Over 30 years, the study estimated over $4 million of projected expenditure, just to keep the place from falling over. I’m not talking enhancements—this is basic stuff like concrete repair and paint.

Predictably, not a single dollar—nothing—had been set aside for this. We were living hand-to-mouth, managing crisis-to-crisis, papering it over with special assessments, and vendor debt kept off the books.

They say the only certain things in life are death and taxes, but whoever said that never ran a city—they forgot wear and tear. Concrete spalls, roofs cave in, pipes break. Bit by bit, until major disasters—Arecibo and Oroville come to mind—occur.

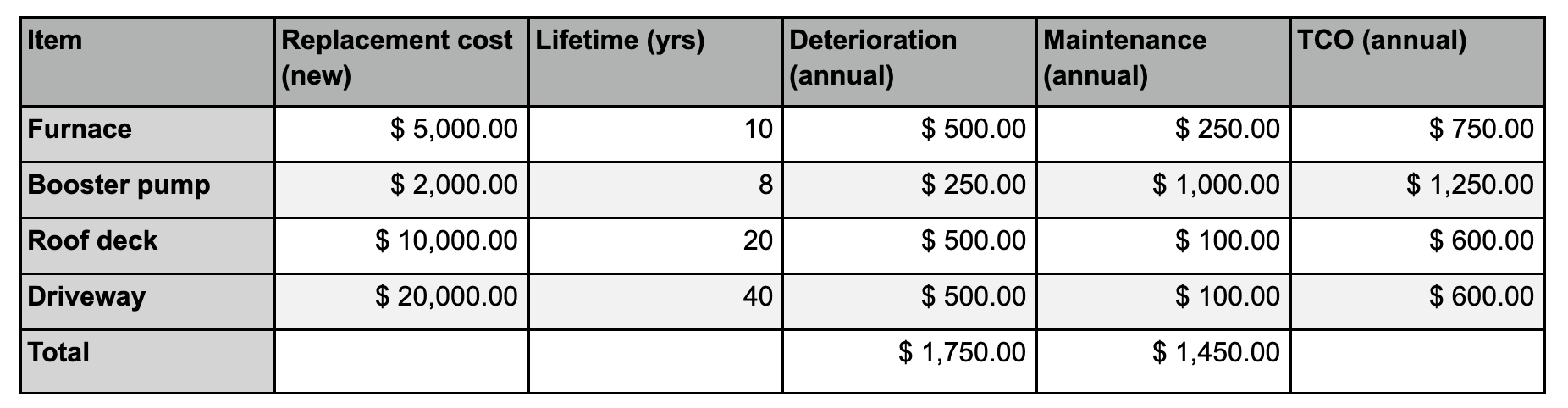

I’m sure this makes me sound fun to hang out with at parties! But really, how hard is this—just make a chart like this:

“TCO” is “total cost of ownership,” the item’s all-in cost, in this case, per year.

If you make this chart, a few things become obvious:

You’re going to need to spend $1,450 annually—every year—on maintenance.

You need to put $1,750—note, a larger amount—into a replacement fund, so that when the time comes, you’ll have the money ready for major component replacement.

Spend $1,450 annually, save $1,750. Really, how hard can this be?

And yet, so many towns, condos, and projects get over their skis. Why?

What goes wrong

I sometimes joke that City Center Plaza is my applied political science laboratory—most people know each others’ names, but it’s also big enough to observe tribalism, parties, and other emergent political behavior. And so, what happens that makes long-term planning so difficult?

A few things. First, “replace” vs. “one more year” is never clear-cut. The furnace with a ten-year life becomes 12, and then 14…rolling the dice, with progressively worse odds, until a major unplanned blow-out occurs. And let me tell you, if you can’t afford to fix it on plan, you definitely can’t afford emergency maintenance.

Drone photo of the author’s new home. Photo courtesy of the author.

Second, accumulating funds for replacement in advance requires stockpiling cash and not touching it, which requires real discipline. The Federal Government couldn’t do it; rather than real estate, stock, or other economically productive assets, the entire Social Security Trust—the program responsible for paying millions of old-age and disabled Americans more than $1 trillion annually—is backed by nothing more than Treasury debt, that is, claims on future taxpayers.

In my example above, the organization would need to sock away $1,750, every year, no excuses, come pandemic, debt crisis, or whatever else life serves up. Rightly or otherwise—this does seem to be something that varies across political systems, cultures, and time—Americans in 2021 seem unable to subordinate long-term goals to the crisis of today, whether deficit-exploding tax cuts, well-intentioned but costly disability access rules, or just giving staff raises. Long-term fiscal health doesn’t seem to be the priority.

In the end, if “politics is the art of the possible,” as they say, the only solution might be to replace things all the time—continuously—a little bit at a time, so that there’s never room in the budget for can-kicks. If your roads last 20 years, you replace 1/20th of them each year. Ditto for water pipes, housing projects, or other major public infrastructure. If you can’t afford to replace a little bit today, guess what, you’re hosed. Time to scale back. No amount of debt, no bailout, no “growing your way out of it” or “pension bonds” or other accounting gimmickry is going to save you.

The good news is, when you replace things a little bit at a time—or do anything often, really—you get better at it. I’ve witnessed it firsthand: organizations that roll their infrastructure over on a regular cycle develop hard skills in project management and estimation, as well as developing a “culture of investment” that prioritizes long-term thinking and goal-setting. Eventually, the reality sets in that “tomorrow never comes”—the cure to deficits is rarely more building, and some things may need to be retired, or downsized.

The backlog

Drone photo courtesy of the author new’s home. Photo courtesy of the author.

This is where we get to borrow a tool from software development: the backlog.

A backlog is nothing more than a list of stuff to do. But they have properties useful to us.

One, you do what’s on top first. Five-year plans are great, but all that matters today—this week/year/quarter—is what we’re doing now. What we do one, two, even five years from today is just a guess.

Second, backlogs constrain. Whether big or small, short- or long-term, our capacity to invest is fundamentally finite—a function of tax revenues, association dues, even sales. Space for 20 things means the 21st gets cut. A budget of $1 million means that after that money is gone, the next item doesn’t make the cut.

And third, backlogs are endless. They go on and on. Just because we aren’t doing something this year, doesn’t mean we won’t do it next year. It just has to wait.

So here’s what you’re going to do. Estimate how much you can afford to spend, every quarter/year, and build a backlog. If you don’t know how much you can spend, guess.

What goes first? Rank it by priority.

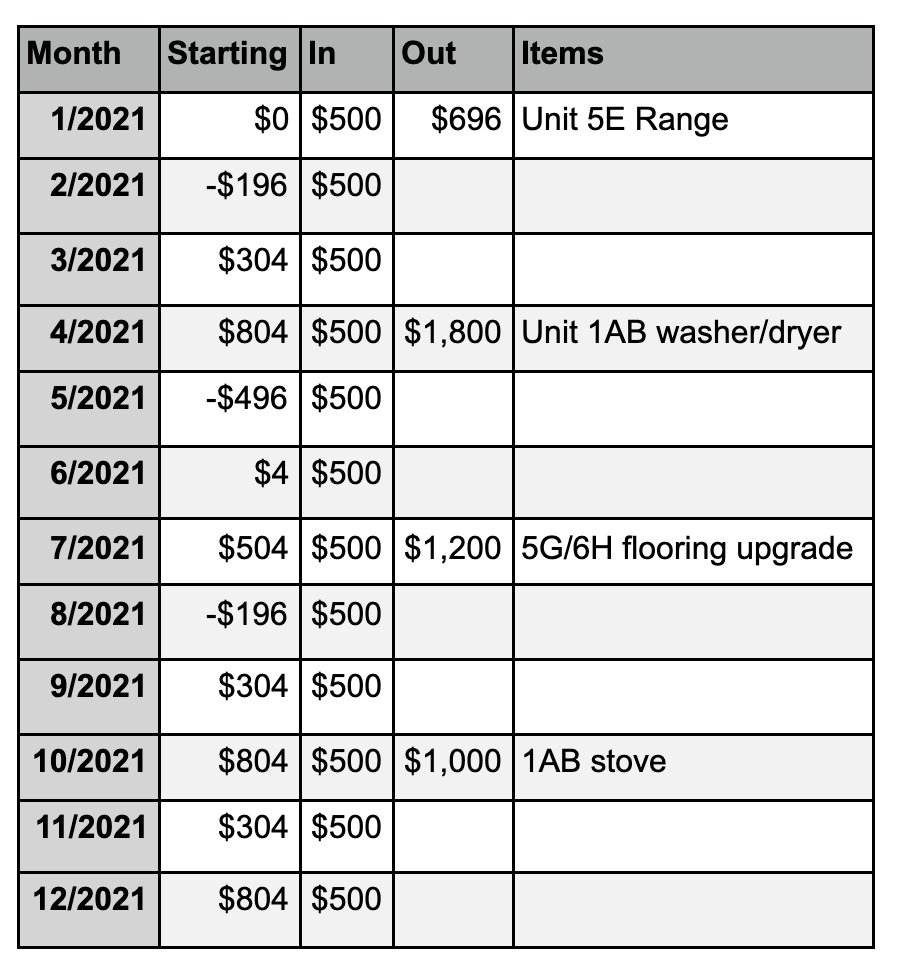

Here’s a real-world example, from an apartment I own.

I paid $425,000 for the apartment. When I bought it, it was in OK but not great condition. My initial estimate was 1-2% per year of the purchase price into capital spending and repair—somewhere between $4,250 and $8,500 annually. I made a guess of $6,000/year because it was near the midpoint, and worked out to a round number each month ($500).

Now it’s time for some hard choices. One guy asked me to fix his carpeting. One of the dryer lines had its exhaust routed into the crawlspace, causing the wood to rot. The water heaters are 30+ years old, the second-floor service walkway needs to be replaced, and the screen doors are falling apart.

I only have $6,000/year to spend. Some things will have to wait—some people won’t like that. Backlogs help you pace investment sustainably, or let you know you’re falling behind—they’re mechanistic, brutal, but ultimately honest, like a fitness coach’s stopwatch, or counting calories.

If you build a serious cashflow analysis like this out over 10-20 years, you’ll get a real sense of what your condo, apartment complex, school district, or town can and can’t afford.

Here’s what I like about my five-column chart:

It’s really simple. Any sixth-grader with a four-function calculator can get it.

It estimates capital expenses in an empirical, bottom-up manner. I didn’t initially know whether $6,000/year ($500/month) was right. After modeling my spending for a few years, it feels like that’s in the ballpark.

It recognizes that priorities change. Planning has value, but sometimes an item just can’t wait. But when it can’t, something else can—something must.

By spreading spending and avoiding the need to hold large sums of cash, it solves the “hands in the cookie jar” problem, of lacking the discipline to hold cash.

It even works with debt. Debt, to me, is like a toddler eating dinner: you can push cashflow around on the plate all you want, but eventually you’ve got to eat it. In this example, I might have to borrow in July (note the “starting” goes negative). But that’s OK, because I have the cashflow (financial capacity) to service it.

It champions smooth, non-bursty spending, leading to the sort of incremental development championed by Strong Towns. You’ll also learn to embrace constraints, and think longer-term.

It forces tradeoffs. If you never get around to replacing or repairing something, perhaps you don’t really need it. When it comes to good intentions, I like to keep the following quote from Warren Buffett in mind: “A check is what separates a conversation from a commitment”. If you can’t write a check, maybe something isn’t a priority after all.

About the Author

David Albrecht is CEO of Dials, the online hub for logging, planning, and publishing all things maintenance. Inspired by Strong Towns, David is also a part-time developer, and owner/operator of missing middle housing via Unchecked Capital, LLC. When not working, David and his ten-month old daughter “devour” the news (The Economist and San Francisco Chronicle) in their own way: he reads it, she eats it. You can connect with David on his website and on Twitter at @davidalbrecht.