Shut Out of Housing Gains

Pete Saunders is a planning consultant and journalist based in Chicago. He blogs at The Corner Side Yard, and we've featured his work a number of times before on Strong Towns. He recently shared an account on his blog that is at once more personal and anecdotal than much of his work, and yet extremely illuminating.

In "A Personal Segregation Story," Saunders uses his own family history to shed a critical light on the notion, pervasive in American society, that homeownership is a path to building generational wealth. He reminds us that for many Americans—and disproportionately for Americans of color—it never has been so:

The neighborhood of my childhood home... is still the home of some of the neighbors I remember from nearly 40 years ago. But in part because of segregation, and an overall moribund regional economy for the last half century.... the neighborhood has remained at a weird level of stasis for a very long time; it looks exactly the same in 2018 as I remember it in 1978. The sense of stasis is reflected in the minimal appreciation in home value. My parents bought it in 1968 for $17,500 and sold it in 1981 for $36,000. Zillow's zestimate for the home today is $72,100.

There was no transfer of generational wealth from my parents to me and my siblings.

In fact, Saunders writes, his parents' home has appreciated at less than the rate of inflation over fifty years. It has been a net money loser, even before the cost of ongoing maintenance of the structure is factored in. And there are millions of homes like it across America.

A common theme in discussions of racial segregation in American housing is the racial homeownership gap—the difference between the rate of white and non-white (especially black) households who own their homes. This gap exists everywhere, and, in the worst cities, is a shocking 50 percentage points. This is a problem because homeownership is the primary vehicle of retirement savings for many, many people, not to mention a source of wealth that can be passed on to their children, used to pay for education and other opportunities.

And yet, the story Saunders is telling is different, and equally troubling. His grandparents were upwardly mobile and were not shut out of homeownership. They owned their homes, on both his mother's and father's side:

All of my grandparents took full advantage of living in the boomtown that Detroit was at that time, particularly in the post-World War II period. There were plentiful employment opportunities in Detroit's manufacturing economy. My mom's dad worked at a Uniroyal plant, through the Depression and beyond. He and my grandmother raised seven children (my mother is the youngest), and they were able to buy a home in the early 1950's near Mack and St. Clair on Detroit's East Side. Like so many homes in Detroit, their house is gone. They lived on one of those Detroit blocks that have become famously abandoned.

His parents owned homes and enjoyed some measure of upward mobility, too:

There was no transfer of generational wealth from my grandparents to my parents.

But that's fine. Both of my parents were still able to parlay their working class/middle class upbringings into becoming first-generation college graduates. They met at Wayne State University in the early '60s and got married and had a child (me) in 1964. We lived not far from where the Detroit riots started in 1967, my earliest memory. With another child, my sister, on the way, they elected to get out of the tense environs near the riot's epicenter and buy a house in a more stable and comfortable area.

They bought a house on Manor Street on Detroit's Northwest Side.

This was the house that, we've already learned, has appreciated at less than the rate of inflation (i.e. it has depreciated in real terms), even though the neighborhood has not hit rock-bottom the way more infamous parts of Detroit have.

Saunders's piece is worth reading in full; it contains much more detail about the homes and neighborhoods of his parents and grandparents, and the experiences they had as black Americans trying to partake in the American dream.

But this story of decline exists all over America. And, although race is central to the story in many places, it also transcends racial politics, and involves motivations and decisions that can't all be chalked up to simple prejudice.

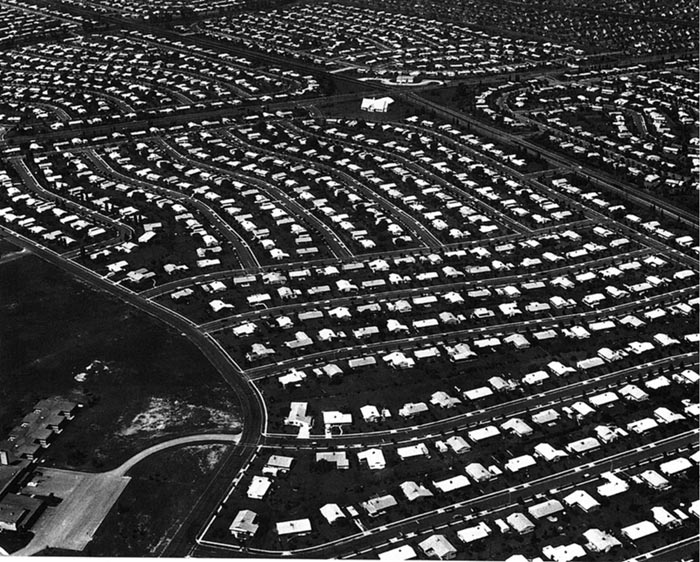

At Strong Towns, we would argue that this story is, in substantial part, the story of the cataclysmic decision we made as a society to embark—everywhere and all at once—on what we call the Suburban Experiment. In the decades following World War II, we threw out a tried-and-true approach to building places that could accrue and retain wealth on a collective level. Instead, we opted to chase the sugar high of short-term growth. We federally subsidized the rapid expansion of new suburbs through mortgage insurance, the GI Bill, and massive top-down investments in transportation infrastructure—the Interstate Highway System—to make these new suburbs easily accessible to jobs in the old urban cores.

In some places, we embarked upon this project with such abandon that we doubled—or more—the amount of land and infrastructure serving the same number of people. It was, as Jason Segedy observes, as if we had built whole duplicate cities next to our existing cities and decamped to them, while promising to somehow find the resources to continue to maintain both.

The staggering growth of Levittown, PA, one of four prototypically suburban "Levittowns" built in the early 1950s. Source: Wikimedia Commons

In doing this, the wealth that accumulated in new suburbs was not all created out of thin air. Yes, there were productivity gains to be had from the surge in construction jobs, and from the added mobility that the freeways represented. But much of the suburbs' newfound wealth was simply cannibalized from the older, intact neighborhoods of our cities and towns.

As the Levittowns of the world boomed, the South Bronxes of the world went into freefall. The suburbs were the beneficiaries of a colossal net transfer of resources out of America's legacy cities and neighborhoods. There is a direct line between suburban expansion and the way people like Pete Saunders's relatives were denied the opportunity to build generational wealth and pass it to their children and their children's children.

There's an important lesson here about the difference between the illusion of wealth—in a place where the pavement hasn't started to crack yet and the maintenance bill hasn't come due—and real wealth. There's also an important lesson about the difference between collective wealth and individual windfalls.

Central to the Strong Towns message is the idea that we need to build and inhabit productive places—places that produce enough excess wealth to make it financially feasible to maintain, in perpetuity, the public infrastructure that supports their existence. It might be tempting to conflate places that build community wealth with the American ideal of homeownership as a path to building individual wealth, and, thus, with the concern for keeping property values high in the short term that motivates much of local political activism by homeowners.

But a place that builds sustainable collective wealth may have very different characteristics than a place that is a springboard to individual wealth.

“But much of the suburbs’ newfound wealth was simply cannibalized from the older, intact neighborhoods of our cities and towns. As the Levittowns of the world boomed, the South Bronxes of the world went into freefall.”

Those who bought into 1950s suburbs in the 1950s (a.k.a. when they were still shiny and new) and sold a few decades later reaped a windfall. Their homes helped finance their retirement and their children's futures as well. Our astute friends at City Observatory have described this transfer of wealth from the young to the old as a "gerontopoly".

Many of the earliest suburbs are now themselves centers of concentrated poverty and economic stagnation. Places like Ferguson, Missouri, which we've written about as a place that epitomizes first-generation suburban decline, have fallen steeply from their mid-century glory days. The first generation of homeowners who used Ferguson as a springboard to build their own, personal wealth are largely gone. They cashed out, many of them in retirement. Can you blame them?

Places that are part of the Growth Ponzi Scheme are hard-wired to decline—in large part because they're built to a finished state, not to incrementally evolve to meet the needs of each successive generation that inhabits them. But these places only do a great job of building the personal wealth of those who are in a position to own the property while it's on the upward part of its trajectory, and sell before the downward swing hits full force.

For a huge range of cultural, sociopolitical, and legal reasons, white Americans have historically been much more likely to be in that position. Black Americans have been the least likely of all racial and ethnic groups to be in that position.

What might the disparities in wealth within American cities look like today if we hadn't embarked on the Suburban Experiment? If, instead, we had let our cities mature while growing slowly and incrementally outward, upward, and more dense? Those with means would not have so fully abandoned older neighborhoods, which instead would have retained more of their intrinsic advantages and economic productivity.

We would have sacrificed homeownership as a means for some to realize windfall investment gains which beat the market as a whole—a dream which, as a matter of simple math, was never going to be available to everyone. (All the children can't be above average, even in Lake Wobegon.) Some people were always going to be shut out of the gains.

But in exchange, more people could live in dignity in homes that provide a source of stability, and access to complete neighborhoods. Our communities could slowly and steadily become more prosperous and secure places over time. And people like Pete Saunders's parents and grandparents, who did so much right in their lives and careers, might have been able to pass on more of what they worked for to the next generation of their families.

That is the true power of a Strong Towns approach.

(Top photo source: Google Earth)

A 2020 study revealed that areas around streets named after Martin Luther King Jr. are more segregated and poorer than the United States average. Now, data shows property values in these areas are affected, as well.