Tremors v. Earthquakes, Banks

I suspect there are very few people outside of Wall Street and Washington DC who believe the consolidation of banking into a handful of too-big-to-fail institutions is a positive development. To build on yesterday's tremor versus earthquake analogy, what we (arguably) gain in efficiency we lose in resiliency. The memory is seared into my brain of Hank Paulson, George W. Bush and Nancy Pelosi telling us that, if we didn't come up with nearly a trillion dollars to save these large banks (it has turned out to be much, much more), there wouldn't be food on the shelves for three days nor money in any ATM.

That can really happen?

Yes, in a system lacking resiliency, one reliant on a handful of fragile players subject to making (and losing) huge bets all backstopped by a volatile political system, it is not hard to imagine a series of moves that leaves us without food and cash, at least for a while. That we've allowed -- indeed perpetuated -- such a distorted and dangerous system is a sign of deep dysfunction.

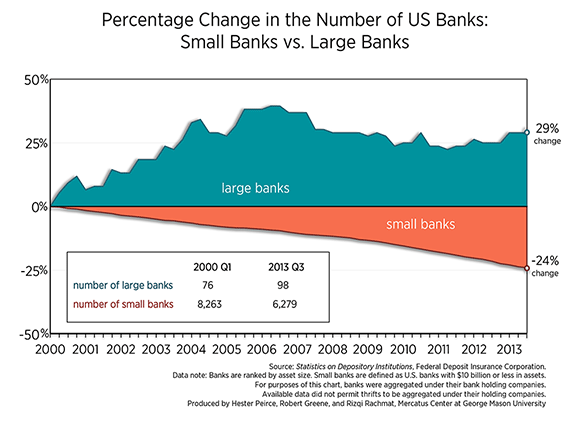

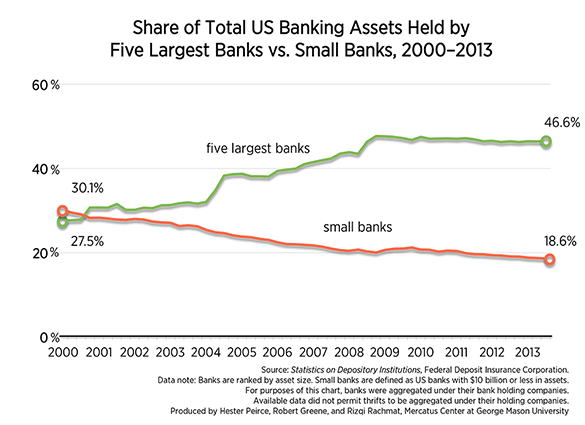

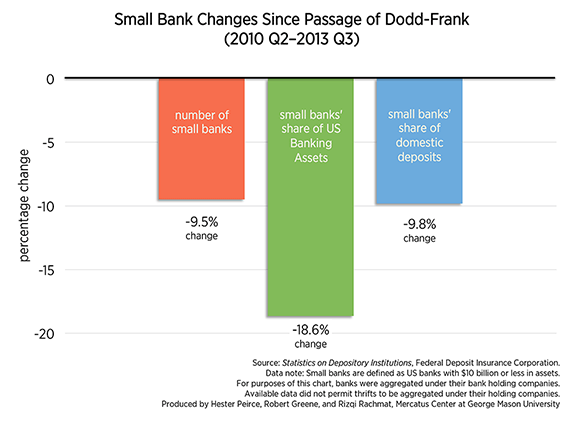

A group at George Mason University published a handful of charts that show how the consolidation of banking continues, despite the earthquake we experienced in 2008.

A small bank here is an institution with $10 billion or less in assets.

I remember back in 2009, the early days of the Obama administration, when Rahm Emanuel, the president's chief of staff, was citing the financial crisis as an opportunity for reform that should not be wasted. Out of that urgency, we got Dodd Frank, an evolving set of regulations that have done little to address the underlying problem.

I've told the story before, but it bears repeating for all our new readers. When I got out of graduate school and was starting my own planning firm, I needed a loan for some equipment and for cash flow. I went to one of the local branches of a too-big-to-fail bank -- the one that had my checking account, savings account and mortgage -- and was thrice denied. I couldn't even get a small loan for equipment, despite having signed contracts and three years of profitable operations. I didn't meet their criteria for whatever reason, but the local banker couldn't really even explain why. He just had a printout.

Then I went to a local bank. (For those of you interested, the local bank is Blackridge Bank here in Brainerd, MN.) Not only did we sit down and go over the entire operation, and not only did I get the loan, but the loan officer actually started coming to our board meetings, providing us financial advice and input as my partners and I got our business up and running.

There is no question that large corporations and franchise-affiliated companies can secure financing in the current system. If we want the type of robust, incremental growth that is going to help us build a nation of strong towns, we need more local banks, not fewer.

You really should be a member of Strong Towns. Join us today and get an invitation to our next big event. Details coming shortly.